What’s an exchange fund?

What you'll learn

- What exactly is an exchange fund?

- How does an exchange fund work?

- What are the benefits of an exchange fund?

- A closer look at the tax benefits of exchange funds

- Who are exchange funds for?

- Exchange fund providers that can help you learn more

If you've amassed significant stock in a single company, you'll encounter difficult choices down the line. You might consider selling the stock to broaden your holdings, yet this could lead to significant tax implications. Alternatively, retaining the stock means enduring the daily fluctuations of having your wealth concentrated in one asset. Exchange funds offer a solution that combines both options. They enable you to diversify your portfolio while also deferring substantial tax liabilities

It's easier than you might imagine. Within minutes, you'll grasp all the essentials about exchange funds and how they can assist you in constructing a more robust portfolio.

What exactly is an exchange fund?

Exchange funds aggregate stocks from numerous investors and consolidate them into a unified fund, granting each investor a share in the fund. This approach enables investors to diversify their holdings without offloading stock and incurring taxable events.

Exchange funds have been utilized to mitigate concentration risk in a tax-efficient manner since the 1930s, though they are not a recent innovation. Historically, these funds were exclusively accessible to ultra-wealthy investors through prestigious investment banks. They are commonly referred to as swap funds, as they enable investors to "swap" a concentrated stock position for a diversified portfolio.

A standard exchange fund comprises stocks contributed by its investors, alongside a minimum of 20% "qualifying assets," such as real estate, mandated by the tax code. These funds are frequently organized to pursue specific investment goals, such as mirroring prominent market indexes. For instance, the Wealth Farming Exchange Fund is tailored to replicate the long-term performance of the Nasdaq-100 index.

An ETF (exchange-traded fund) is a fund available for purchase and sale on public exchanges. These funds typically contain a basket of stocks and/or bonds aligned with a specific investment objective. Investors can acquire ETFs using their funds through most brokerage platforms.

An exchange fund is a tax-efficient private fund possessed by investors who swap their individual stock for shares in the fund. These funds solely accept "in-kind" stock contributions, rather than monetary investments. Additionally, shares in the fund are not tradable on public exchanges.

The understandable confusion between "exchange fund" and "ETF" stems from the distinct meanings of "exchange" in their respective names.

How does an exchange fund work?

Consider an example to illustrate how an exchange fund can advantage investors. Let's envision four veteran employees of technology firms who have accumulated highly appreciated stock:

While we've used a small group of investors in this example for simplicity, exchange funds typically encompass a much broader portfolio tailored to fulfill specific investment objectives.

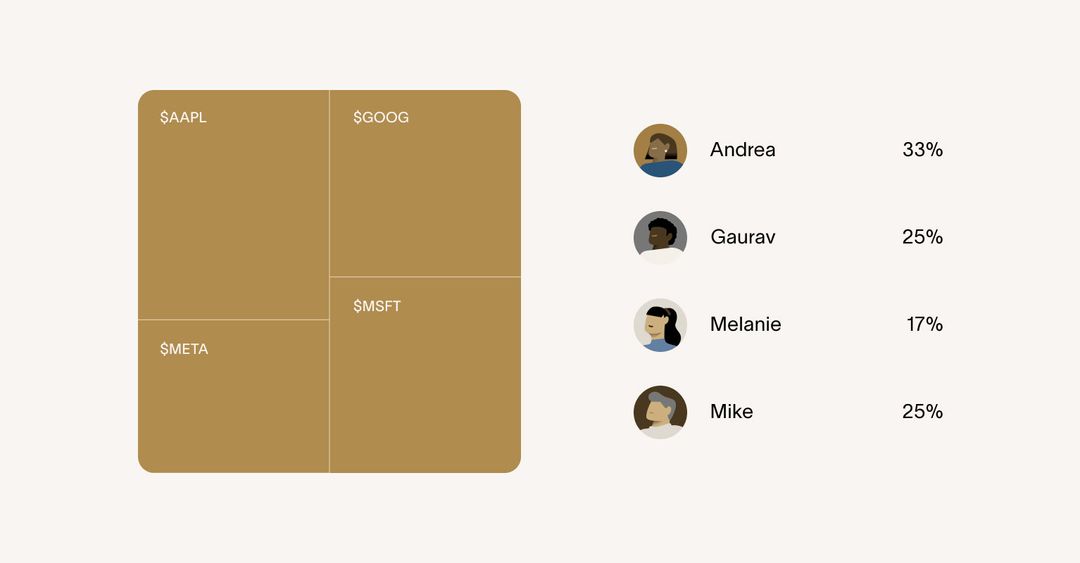

Now, envision these investors consolidating their holdings to establish an exchange fund. By collectively engaging in an exchange fund, they could defer capital gains taxes while diversifying their investments away from their appreciated positions.

Instead of owning individual stocks, each investor would possess a share of the fund commensurate with their initial contribution:

Furthermore, each investor's stake in the fund remains constant, irrespective of the performance of the stock they contributed. They are now invested in the fund itself rather than the underlying stock.

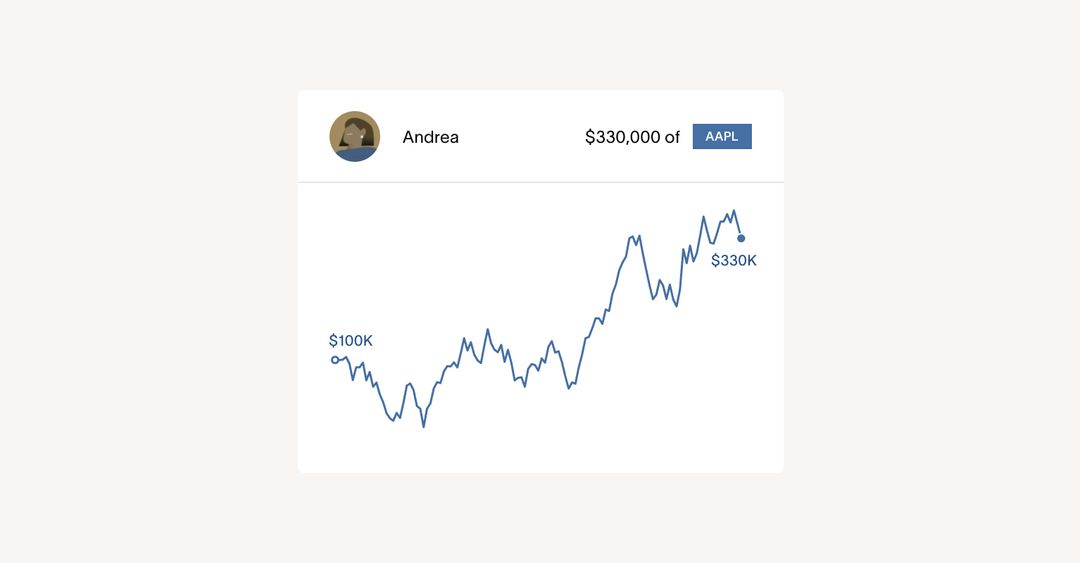

To qualify for tax-deferred treatment, current tax regulations mandate that investors retain their investment in the fund for a duration of seven years before they can access their diversified basket of stocks. Upon selling those stocks, the original cost basis remains applicable. For instance, Andrea's $100,000 cost basis would ultimately determine her capital gains.

This serves as a basic illustration. If you wish to delve further into the historical, regulatory, and technical facets of exchange funds, explore our comprehensive guide detailing how exchange funds operate.

What are the benefits of an exchange fund?

By facilitating the withdrawal of your winnings without activating capital gains taxes, exchange funds can assist you in:

-

Diversify your portfolio and mitigate risk.

Transition from a concentrated portfolio (comprising more than 10% of your net worth in a single asset) to a diversified portfolio meticulously aligned with an investment objective. While all stocks experience fluctuations, a basket of stocks is less prone to losing most or all of its value compared to stock in a single company significantly underperforming. It's important to note that diversification does not assure investment returns and does not eliminate risk.

-

Minimize tax drag

Realizing capital gains on your stock and paying taxes on them leaves you with less money to invest, a phenomenon known as tax drag. This can impede the long-term growth of your portfolio. However, an exchange fund allows your initial investment to continue appreciating by deferring taxation. Check out our comprehensive guide to learn more about tax drag.

-

Embark on a fresh journey.

A concentrated position often arises from hard work, astute decisions, and good fortune. It's natural to develop emotional attachment to the single stock driving your portfolio. Exchange funds alleviate many reasons for maintaining all your investments in one basket by postponing taxation and diminishing volatility.

-

Mitigate the risk tied to your employer.

If you're employed at a company and maintain a concentrated position in its stock, you're doubly exposed to the business risk of that company. Diversifying your holdings mitigates the financial risk if the company encounters business difficulties.

-

Maximize tax efficiency

Rather than being compelled to liquidate when you're in a high tax bracket, exchange funds afford you the opportunity to diversify now and retain control over when you liquidate your stock, if ever. You can alleviate your tax burden by liquidating smaller portions of your portfolio when you're in a lower tax bracket or passing them on to your heirs.

-

Enhance your estate planning

Exchange funds can offer notable estate planning advantages for specific investors as well. According to the prevailing IRS code, your heirs may have the opportunity to withdraw a diversified basket based on a stepped-up cost basis.

Our exchange fund simulator makes it easy to try on an exchange fund and see whether it might be a good fit.

A closer look at the tax benefits of exchange funds

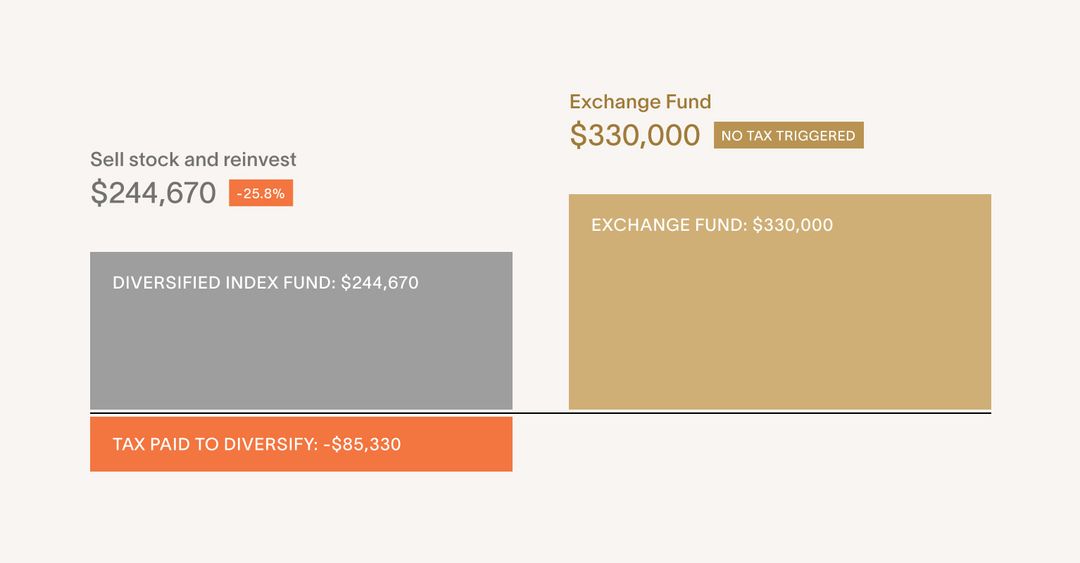

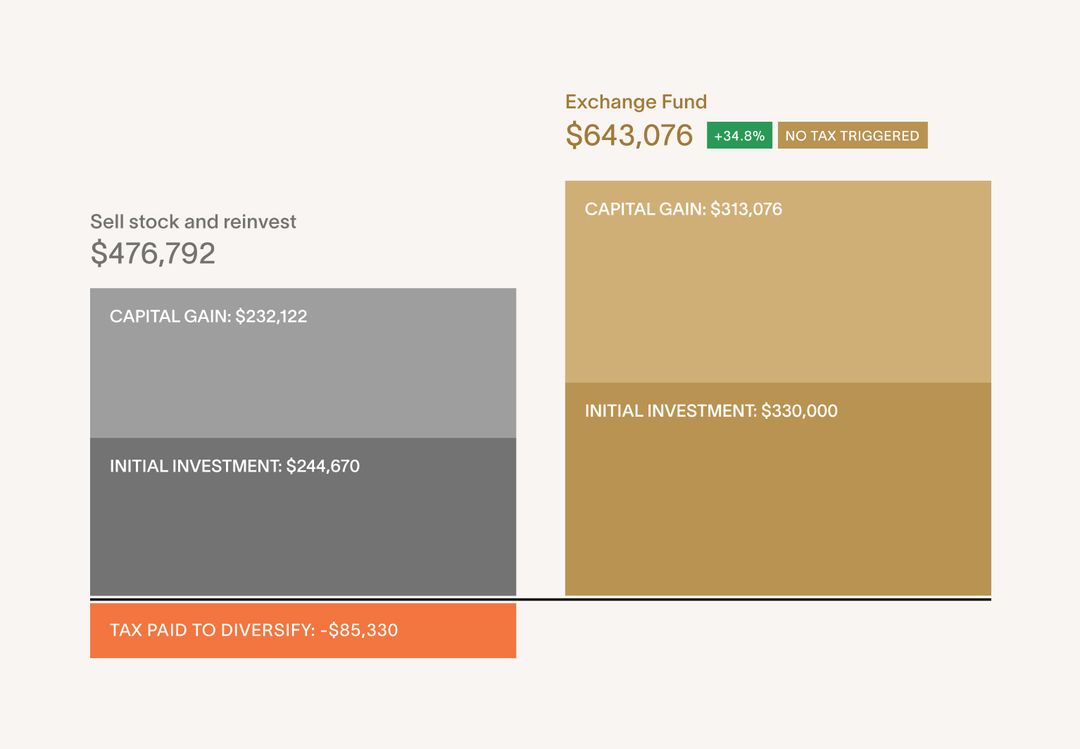

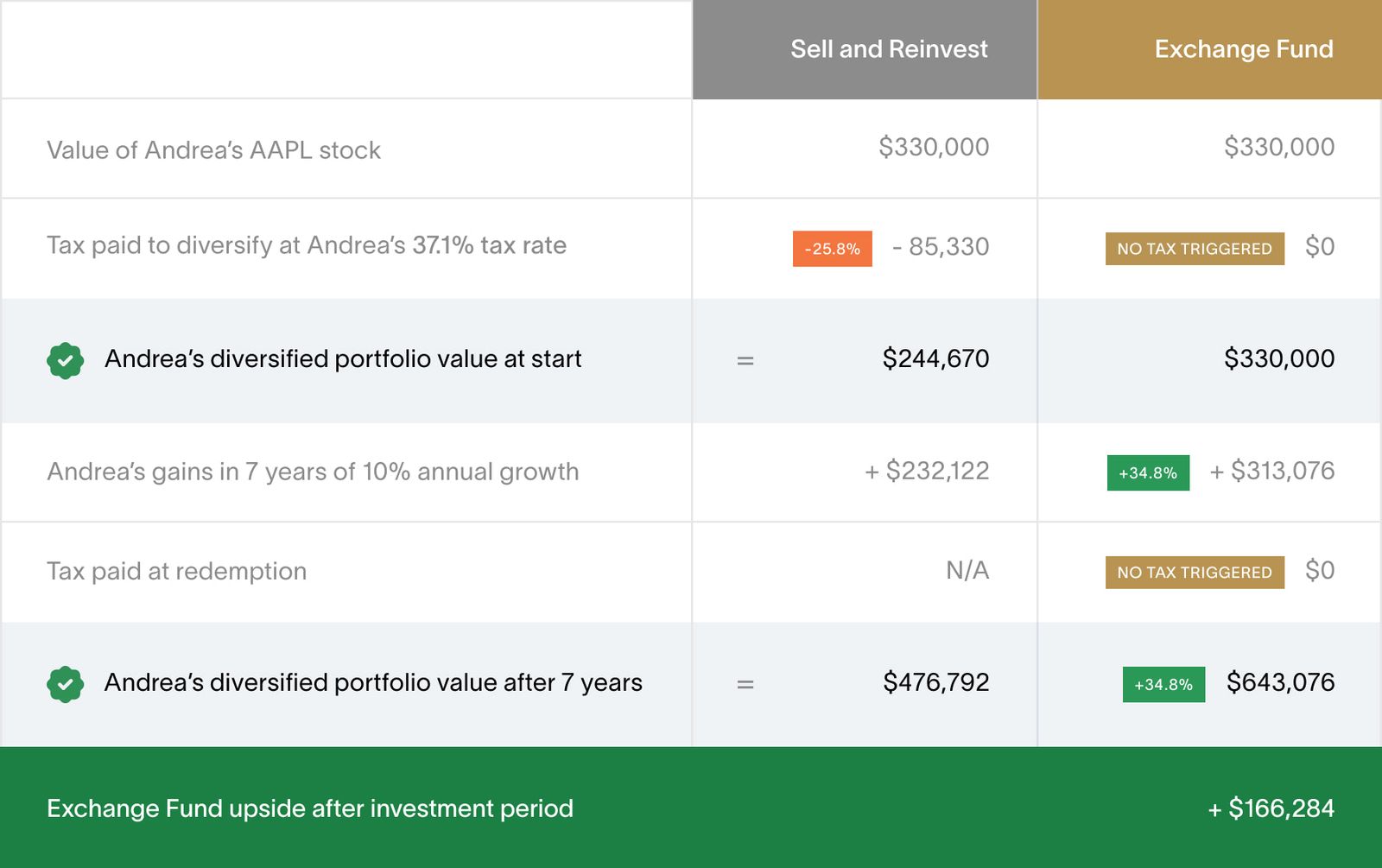

To delve deeper into comprehending the tax advantages and how tax drag can influence your portfolio, let's revisit our example. Remember that Andrea has accrued $330,000 worth of Apple stock as equity compensation, with a cost basis of $100,000.

Here's a theoretical comparison between selling her Apple stock (and paying an effective capital gains tax of 37.1%) versus contributing her stock to an exchange fund:

This illustration demonstrates the outcomes at the initial stage of the investment. With the sell-and-diversify strategy in Scenario 1, you deploy fewer dollars. Despite the inherent market risk in investing, the seven-year holding stipulation allows ample time for compound interest to leverage the larger asset pool in Scenario 2.

If Andrea's diversified assets grow at a rate of 10% per year over the seven-year period, this is her projected outcome:

At the conclusion of the seven-year holding period, engaging in an exchange fund places Andrea approximately 35% ahead of where she would have been if she paid capital gains taxes before diversifying. Moreover, if she were to retain the exchange fund for more than seven years, the potential of compound interest could further widen the performance gap.

Here's the comprehensive performance breakdown if Andrea earns 10% annual returns and sells after seven years (factoring in her 37.1% tax rate):

Explore our exchange fund simulator if you wish to calculate the numbers for an illustration of how these principles could apply to your circumstances. Please bear in mind that these figures are hypothetical and do not constitute a projection or a guarantee of future performance. They are based on several assumptions, detailed at the bottom of our simulator page.

The hypothetical example above does not depict actual trading or consider the influence of significant economic and market factors.

Who are exchange funds for?

Determining if an exchange fund is suitable for you depends on your financial situation and whether you meet the eligibility requirements. Here are four crucial factors to consider:

-

Diversify your portfolio and mitigate risk.

If a substantial portion of your investment portfolio is concentrated in a single stock, particularly one that has appreciated significantly, exchange funds can offer an effective means to diversify your holdings. Are you seeking a method to mitigate risk in a tax-efficient manner? Additionally, are you prepared to maintain the investment for a minimum of seven years? If so, an exchange fund may align well with your portfolio objectives.

It's important to note that all exchange funds, including The Wealth Farming Exchange Fund, entail certain risks, including the potential loss of principal invested in the fund.

- Over $200,000 in annual income OR

- Over $300,000 in annual income, when combined with a spouse or partner OR

- Over $1,000,000 in net worth (individually or with a partner), excluding the value of your primary residence

Certain traditional exchange fund providers may stipulate that participants must meet the elevated criterion of being a "qualified purchaser" with over $5,000,000 in investments.

Additionally, it's important to recognize that providers may have specific requirements regarding the stocks included in their funds. For instance, The Wealth Farming Exchange Fund is composed of stocks mirroring the performance of the Nasdaq-100. To fulfill our diversification objectives, we aim for a well-rounded portfolio that avoids overconcentration in any single stock. Explore how it operates for more details.

-

Who qualifies for participation in an exchange fund?

To qualify for a contemporary exchange fund, such as the one offered by Wealth Farming, you must satisfy the SEC's criteria for an accredited investor. This typically entails meeting one of the following requirements:

-

What is the minimum contribution required for an exchange fund?

Many traditional exchange fund providers typically mandate contributions ranging from $500,000 to $1,000,000 worth of a specific stock to participate in their funds. However, the more contemporary Wealth Farming Exchange Fund permits contributions as low as $100,000.

-

What timeframe are you considering?

When opting to participate in an exchange fund, an investor should both have the intention and possess the financial stability to commit for at least seven years.

If there arises a need to redeem shares in an exchange fund before the completion of seven years, only the original shares can be withdrawn. Additionally, most funds impose penalties for early redemptions, and there are lockup periods for a certain duration after the fund's initial creation.

For investors with a shorter time horizon, investment vehicles such as a collar advance or stock lending might offer a more suitable method to capitalize on a concentrated stock position.

To qualify for tax deferral, adherence to the seven-year duration within the exchange fund is essential. Exchange funds serve as a long-term financial planning tool designed to facilitate diversification of holdings.

What are the downsides of an exchange fund?

For investors possessing a concentrated position and adopting a long-term investment strategy, exchange funds offer numerous advantages. Conversely, the drawbacks of exchange funds typically pertain to individuals with shorter-term time horizons or low-risk tolerance due to:

- Restricted liquidity: To leverage the tax benefits of an exchange fund, you are required to maintain it for a duration of seven years. Redeeming before this timeframe undermines the purpose of utilizing one. However, it's worth noting that you could opt to borrow against your fund shares if liquidity is required – though it's essential to acknowledge that borrowing against fund shares entails added risks.

- Investment limitations: An exchange fund functions as a passive investment instrument crafted to offer diversified exposure aligned with a specific investment objective. Typically, exchange funds refrain from selling contributed stocks due to unfavorable tax implications, thereby potentially limiting the ability to rebalance the portfolio as assertively as with other investment vehicles such as ETFs.

- Tax laws may undergo changes: The advantageous tax treatment of an investment in an Exchange Fund is contingent upon existing tax regulations. Although the benefits might be preserved under any new tax laws, retroactive treatment is not assured in the event of changes to tax laws.

Exchange fund providers that can help you learn more

Many traditional investment banks and wealth advisors offer exchange funds or similar services to their clients. However, these services typically cater to qualified investors with assets exceeding $5 million. It's advisable to verify eligibility and requirements with individual providers.

Conversely, The Wealth Farming Exchange Fund presents a contemporary approach to these funds with fewer restrictions. If you possess a concentrated position of over $100,000 in a publicly traded company, we invite you to reach out to us. Inform us if you have a concentrated holding and are interested in learning more!

Disclosure

Material presented in this article is gathered from sources that we believe to be reliable. We do not guaranteed the accuracy of the information it contains. This article may not be a complete discussion of all material facts, and is not intended as the primary basis for your investment decisions. All content is for general informational purposes only and does not take into account your individual circumstances, financial situation, or your specific needs, nor does it present a personalized recommendation to you. It is not intended to provide legal, accounting, tax or investment advice. Investing involves risk, including the loss of principal.